Eq: Total Market

Most investors would rather go to the dentist than take a look at their portfolios this year. 2022 has been a tough year for investors with both the equity and the fixed-income markets experiencing large drawdowns. Unless you’ve been all in on commodities this year, your portfolio has likely taken a hit.

This has been especially true for investors with large exposure to technology stocks. The Technology Select Sector SPDR ETF (XLK), which tracks the technology sector, is down 28% through October 21st. Out of the eleven SPDR Sector ETFs, only the Real Estate Select Sector SPDR ETF (XLRE) and the Communication Services Select Sector SPDR ETF (XLC) are down more.

But who could blame an investor for a large technology allocation, especially with the way tech stocks had been performing over the last five years? Even during the last major selloff at the beginning of the COVID pandemic, the technology sector held up better than most sectors. However, this year, tech stocks have been anything but strong performers.

It’s not just technology either, all sector leadership has changed considerably over the past twelve months. At the end of the third quarter last year, consumer cyclicals, technology, and financials, ranked first, second, and third in the DALI sector rankings, while utilities, energy, and consumer staples ranked in the bottom three.

Fast forward to the third quarter this year, and energy, consumer staples, and utilities held the top spots, while technology, consumer cyclicals, and financials ranked in the eighth, tenth, and fourth spots.

Looking at the period between September 30, 2021, and September 30, 2022, a hypothetical equal-weighted portfolio consisting of the top sectors in Q3 2021, the Technology Select Sector SPDR ETF (XLK), the Consumer Discretionary Select Sector SPDR ETF (XLY), and the Financial Select Sector SPDR ETF (XLF) would have lost 20.06%, underperforming the S&P 500 by almost 3.5%.

But an equal-weighted portfolio made up of the top sectors in Q3 2022, including the Energy Select Sector SPDR ETF (XLE), the Utilities Select Sector SPDR ETF (XLU), and the Consumer Staples Select Sector SPDR ETF (XLP) would have gained 12.58% over the same period, outperforming the S&P 500 by more than 29% and the previous portfolio by 30%.

That hypothetical difference of 30% reflects the cost of assuming that top sectors will remain at the top consistently. If instead, an investor followed a relative strength model and rotated with the market leaders, he or she would have likely been able to avoid those losses.

2022 is also notable as there is a nearly 80% year-to-date differential between the top-performing sector, the Energy Select Sector SPDR ETF (XLE), and the bottom-performing sector, the Communication Services Select Sector SPDR ETF (XLC), indicating that there is, even more, to be gained this year by picking the top sector and avoiding the worst.

The change in leadership and the large differential this year provides a useful reminder that long-term sector trends such as technology can change quickly and investors would benefit from the use of relative strength.

Tap into DALI sector rankings and access more investing tools with a 30 day free trial of Nasdaq Dorsey Wright’s Research Platform.

It’s no secret that many active fund managers fail to beat their benchmarks over the long term, but investor trading activity in those funds is even worse. A Morningstar examination of investor returns in the largest active bond funds revealed self-destructive behavior by investors. According to Morningstar, investors in the 20 largest Intermediate Core Plus Bond funds, which have 10-year records, were so bad over the last ten years that they gave up more return than the Bloomberg US Aggregate index delivered. The average fund returned 2.11% annualized for the last ten years ending in August, while the Bloomberg US Aggregate index returned 1.35% return. Surprisingly, every single one of the 20 funds outperformed the index, but investors were not able to take advantage of this outperformance. Investors lost 75% of the average return the funds delivered, ending up with an 0.53% annualized return. Poor timing can account for the dismal returns for investors. Between 2021 and 2022, investors added $91 billion to the category looking for extra yield over the aggregate index. Unfortunately, this coincided with inflation which led to intermediate-term bond prices falling.

Finsum: Investors poured money into active fixed-income funds at the worst possible time, leading to massive underperformance compared to the funds.

Put it this way: research analysts and model portfolios don’t go hand in hand. Meaning, of course, an analyst can’t provide model services, according to cskruti.com. Nope. None. Nada.

"I have been asked this multiple times by the advisers and my answer has always been “NO!”

In other words: zip.

But why, you might ask. Well, no buy/sell recommendation in a specific security exists, the site continued. While advice on a “portfolio of securities” is covered under Investment Advisers Regulations, that’s not the case under research analyst regulations.

Those existing research analysts dispensing model portfolios must alter the product offering and discontinue offering portfolios. What’s more, when it comes to a specific security where clients can determine the action on a specific security, analysts are able to provide buy/sell recommendations.

Further driving home the point, based on the terms of a settlement order passed by the Securities and Exchange Board of India in May, sebi-registered research analysts are unable to offer either the portfolios or advisory services, according to livemont.com.

It’s expected the settlement will have reverberations on the platform Smallcase. It offers investors curated portfolios and was created by research analysts and investment advisors.

More...

by Thomas Forsha, CFA

Is now the time to be adding dividend-paying stocks to your portfolio? With interest rates moving higher, and deflationary pressures subsiding, the key drivers of growth outperformance over the past decade appear to be stalling.

What seems to be a longer-term shift may support value and higher quality dividend-paying companies versus speculative growth companies.

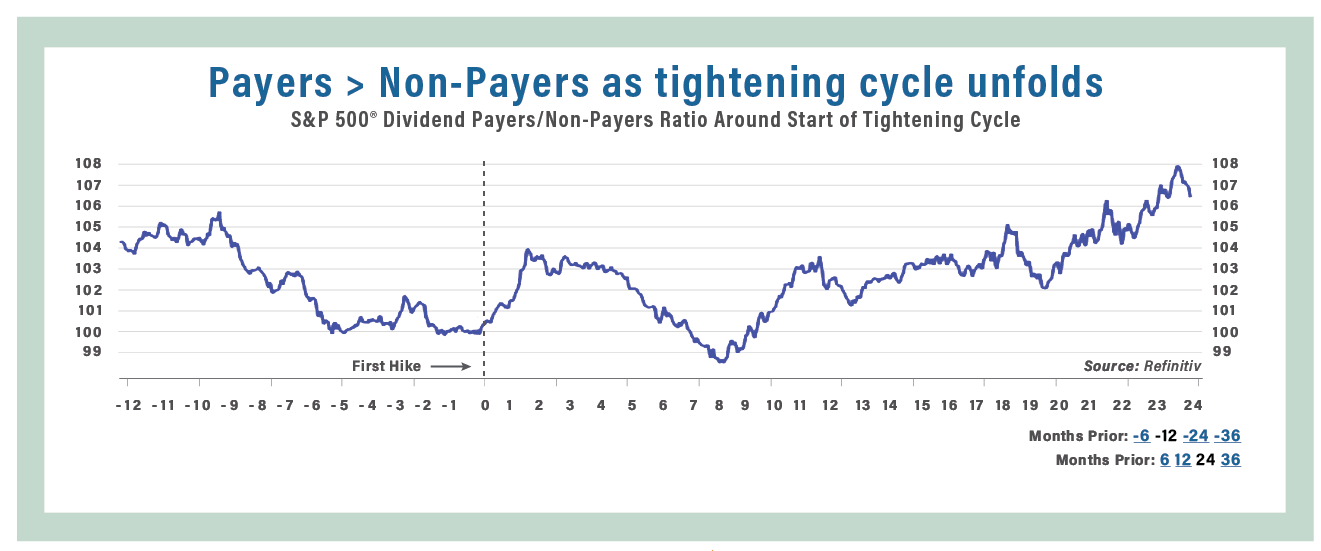

The promise of a dividend check provides an additional dose of certainty for investors. According to Ned Davis Research, dividend-paying stocks in the S&P 500® tend to underperform non-payers in the months leading up to the first-rate increase of a tightening cycle, but in the years after the initial increase dividend payers have outperformed on average by a wide margin. While the past decade has been tough for dividend-focused investors, the best performance for dividend payers has historically been the period that followed the first fed funds rate increase.

Source: Ned Davis Research, Inc. See NDR Disclaimer at www.ndr/copyright.html.

For vendor disclaimers refer to www. ndr.com/vendorinfo/

With interest rates marching higher and the yield curve steepening, Ned Davis Research points toward the potential for the outperformance of value stocks during a rising rate environment. Will the yield curve steepen over the second half of the year as the Federal Reserve is able to successfully manage a soft landing for the economy, or will tightening prompt a recession causing the yield curve to collapse again? Either outcome is likely to prove favorable for the relative performance of value strategies. And historically, the average value stock tends to enjoy higher dividend income than the average growth stock.

Past performance is not a guarantee of future results.

Diversification does not guarantee a profit or protect against a loss in declining markets.

Investing involves risk including possible loss of principal. There is no guarantee that these investment strategies will work under all market conditions, and each investor should evaluate their ability to invest for a long term, especially during periods of downturns in the market.

The S&P 500 Index is a capitalization-weighted index of 500 stocks. The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

This does not constitute investment advice or an investment recommendation.

This represents the views and opinions of River Road Asset Management. It does not constitute investment advice or an offer or solicitation to purchase or sell any security and is subject to change at any time due to changes in market or economic conditions. The comments should not be construed as a recommendation of individual holdings or market sectors, but as an illustration of broader theme.

Data is from what we believe to be reliable sources, but it cannot be guaranteed. River Road Asset Management assumes no responsibility for the accuracy of the data provided by outside sources.

Drop in the, um, bucket list? The performance of a number of model portfolios that leverage the bucket strategy recently was put under a microscope by Christine Benz, Morningstar’s director of personal finance, according to smartasset.com. While the year’s been unkind to the portfolios given their bottom line’s have taken a hit, nevertheless, they’ve outperformed the traditional 60/40 portfolio. That, of course, is an asset allocation retirees commonly use. Further, they’ve outpaced the S&P 500. Through the first six months of 2022, it was down – and by a considerable margin.

The strategy’s a way to spread your assets across different groups of investments that will be tapped at various points.

“[T]he Bucket system has delivered by keeping the faucets open,” Benz wrote. “Retirees using a Bucket system can draw upon their cash reserves without having to disrupt their long-term investments, which have likely experienced price declines so far this year.”

So, is the bucket list holding up in light of the difficulties of the year’s market performance? That would be a resound yes, as it does what it was designed to, according to Morningstar.com.

"True, all of my Model Bucket Portfolios have lost money this year -- and my guess is that most retiree bucketers are seeing red ink for the whole of their portfolios, too,” said Benz. (As of late June, a 60% U.S. equity/40% bond portfolio would be down about 16% for the year to date.)

But the Bucket system has delivered by keeping the faucets open: Retirees using a Bucket system can draw upon their cash reserves without having to disrupt their long-term investments, which have likely experienced price declines so far this year.”

When it comes to September, stocks have a track record of not exactly rocking – much less rolling. For the 30 year period, average returns chime in at -0.34% and -0.26% for the 15-year period, according to forbes.com. The five year period: -0.92%.

And it just keeps getting better with the month in a category of its own as a period when the market held down the rear, drooping on average in every time period.

Now, consider that along with the fact that, already, the year, stoked by factors such as flaming inflation, bulging interest rates and a recession keeping nearly everyone on edge has, you might say, been crackling with volatility. So, how could investors react? Why, they might go shopping for a placeholder for their considerable assets.

Fed chair Jerome Powell, addressing this year’s Jackson Hole Economic Symposium, acknowledged that to stave off growth, it’s probable rates will remain on the high side, not exactly comforting to households and businesses, according to talkmarkets.com.

Trying to read the tea leaves, there are market watchers who believe Powell means he’s no longer homed in on a soft landing. Rather, his focus might on a “growth recession,” as economists characterize it. A growth recession, of course, loosely is marked as a period when the economy’s headed north, yet so slowly that it’s putting a crimp in the volume of available jobs.