FINSUM

StockSnips Launches AI Sentiment-based Sector Model Portfolio

StockSnips, a firm that provides easy access to stock market news sentiment analysis, announced that it has introduced a new SPDR Sector ETF-based portfolio model that ranks sectors by leveraging its proprietary sector sentiment signal. This will be the fifth StockSnips model portfolio that aims to deliver alpha after the launch of equity-based portfolios last year. With model portfolios increasingly attracting assets and markets being impacted by social media, investor sentiment, and chatter, StockSnips believes its signal can quantify those investor sentiment trends, resulting in alpha for end investors. While most sentiment analysis uses a survey methodology, StockSnips separates signals from the noise through Micro-sentiment, focused at the individual firm level. Ravi Koka, CEO of StockSnips commented on the model, "We are excited to bring a sector ETF-based portfolio model to investment advisors and asset managers, leveraging our extensive research in transforming unstructured textual information to a valid signal, and a robust proxy for measuring investor sentiment for a sector.” Their ticker-based portfolio models have performed well so far in a volatile 2022, and they believe the back-testing results for their sector model bode well for investors as well.

Finsum:StockSnips introduced its fifth model portfolio that aims to achieve alpha through its proprietary sector sentiment signal.

What Happens When Inflation Peaks?

Managing Partner and CIO of Renaissance Investment Management

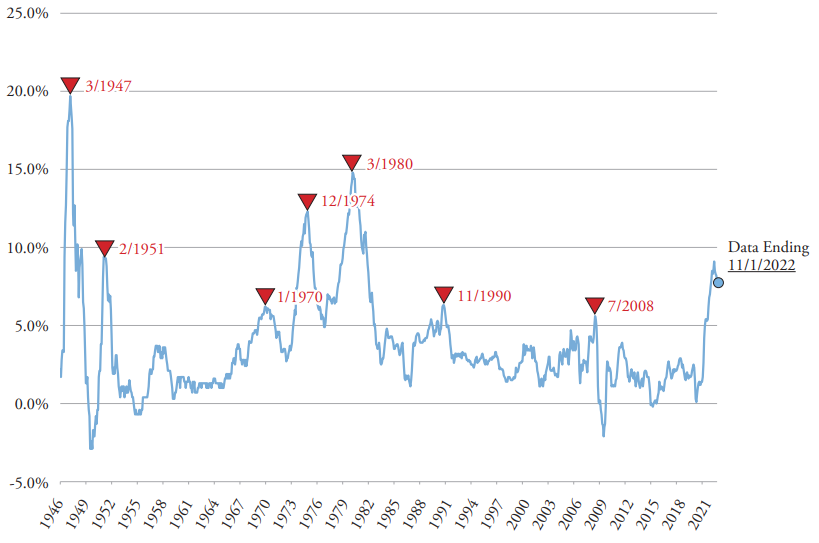

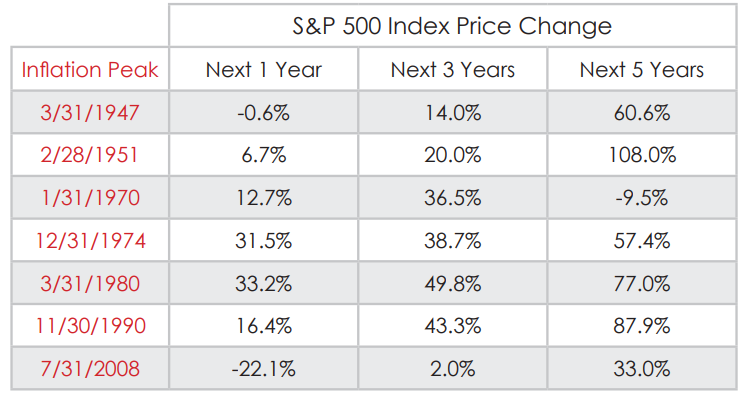

Inflation data through October, released on November 10, showed an inflation rate below most expectations. If inflation has truly peaked and a serious recession is avoided, the historical evidence suggests that stocks are likely to do well going forward.

The Consumer Price Index (CPI) posted a 0.4% rise on a month-to-month basis and a 7.7% change on a year-over-year basis, with the latter being the lowest annual rate reported since January. The core inflation rate (excluding food and energy components) was also below expectations, rising 0.3% on a month-to-month basis and 6.3% on an annual basis.

Rolling 12-Month Change in CPI, 1/1/1946–11/1/2022

Sources: Renaissance Research, FactSet.

Past performance is not indicative of future results. Performance for periods of one year or less is not annualized. All returns are shown in U.S. dollars. Consumer Price Index (CPI) is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item.

Annualized inflation has dropped meaningfully from its 8.5% rate in March. While it may be premature to declare that inflation has passed its highest level, it is still worthwhile to review what has happened in the past to stocks when inflation peaked.

The chart above shows the annualized change in the CPI over the post-WWII era, with peaks in inflation noted (we only marked periods when inflation peaked at rates above 5%, similar to the current environment). The table below shows the price change of the S&P 500® Index over the 1, 3, and 5-year periods after a peak in inflation.

Stocks have generally performed well following a peak in inflation, averaging a 59.2% gain in price five years afterward. The only periods when stocks did not post gains were in periods that included severe recessions, such as in 2008 and 1973-1974.

Stock Market Performance After Peaks in Inflation, 1/1/1946–11/1/2022

Sources: Bloomberg, FactSet.

The risk of a serious recession remains significant, as the Federal Reserve’s strategy of raising interest rates to choke off inflation may choke off economic growth as well. That said, if a serious recession is avoided partly because inflation peaked, historical precedent suggests that stocks are likely to do well in the future.

Past performance is not a guarantee of future results.

This Market Update reflects the thoughts of Renaissance as of November 15, 2022. This information has been provided by Renaissance Investment Management. All material presented is compiled from sources believed to be reliable and current, but accuracy cannot be guaranteed. This is not to be construed as an offer to buy or sell any financial instruments and should not be relied upon as the sole factor in an investment making decision, nor should it be considered a recommendation. The views and opinions expressed are those of the Chief Investment Officer at the time of publication and are subject to change. There is no guarantee that these views will come to pass. As with all investments, there are associated inherent risks. Please obtain and review all financial material carefully before investing.

PERFORMANCE

If Renaissance or benchmark performance is shown, it represents historically achieved results, and is no guarantee of future performance. Future investments may be made under materially different economic conditions, in different securities, and using different investment strategies and these differences may have a significant effect on the results portrayed. Each of these material market or economic conditions may or may not be repeated. Therefore, there may be sharp differences between the benchmark or Renaissance performance shown and the actual performance results achieved by any particular client. Benchmark results are shown for comparison purposes only. The benchmark presented represents unmanaged portfolios whose characteristics differ from the composite portfolios; however, they tend to represent the investment environment existing during the time periods shown. The benchmark cannot be invested in directly. The returns of the benchmark do not include any transaction costs, management fees, or other costs. The holdings of the client portfolios in our composites may differ significantly from the securities that comprise the benchmark shown. The benchmark has been selected to represent what Renaissance believes is an appropriate benchmark with which to compare the composite performance.

The value of an investment may fall as well as rise. Please note that different types of investments involve varying degrees of risk and there can be no assurance that any specific investment will either be suitable or profitable for a client or prospective client’s investment portfolio. Investor principal is not guaranteed and investors may not receive the full amount of their investment at the time of sale if asset values have fallen. No assurance can be given that an investor will not lose invested capital. Consultants supplied with these performance results are advised to use this data in accordance with SEC guidelines. The actual performance achieved by a client portfolio may be affected by a variety of factors, including the initial balance of the account, the timing and amount of any additions to or withdrawals from the portfolio, changes made to the account to reflect the specific investment needs or preferences of the client, durations and timing of participation as a RIM client, and a client portfolio’s risk tolerance, investment objectives, and investment time horizon. All investments carry a certain degree of risk, including the loss of principal, and are not guaranteed by the U.S. government.

REFERENCED INDEX

(Indices are unmanaged and are not available for direct investment.)

S&P 500 Index—The S&P 500 Stock Index is a market capitalization weighted index and consists of 500 stocks chosen for market size, liquidity, and industry group representation.

S&P Midcap 400 Index—The S&P MidCap 400 Index, is a capitalization-weighted index that serves as a gauge for the U.S. mid-cap equities sector.

S&P Small Cap 600 Index—The S&P Small Cap 600 Index is a capitalization-weighted index that measures the performance of selected U.S. stocks with a small market capitalization.

S&P DATA

S&P Dow Jones is the source and owner of the trademarks, service marks, and copyrights related to the S&P Indexes. S&P® is a trademark of S&P Dow Jones. This presentation may contain proprietary S&P data and unauthorized use, disclosure, copying, dissemination, or redistribution is strictly prohibited. This is a presentation of Renaissance Investment Management. S&P Dow Jones is not responsible for the formatting or configuration of this material or for any inaccuracy in Renaissance’s presentation thereof. This data is to be used for the recipient’s internal use only.

Money Managers Falling in Love with Treasuries Again

Even though inflation continues to force the Fed’s hand on tightening, money managers are starting to rebuild their exposures toward Treasuries, with the hope that the highest payouts in years will help cushion portfolios from the damage inflicted by additional rate hikes. For instance, Morgan Stanley believes that a multi-asset income fund can find some of the best opportunities in decades in dollar-denominated securities such as inflation-linked debt and high-grade corporate obligations. That’s because interest payments on 10-year Treasuries have hit 4.125%, the highest since the financial crisis. In addition, PIMCO estimates that long-dated securities, which have been hit hard due to the Fed’s hawkishness, will bounce back if a recession should occur. They believe that a recession would ignite the bond-safety trade, where government debt would act as a hedge in the much-maligned 60/40 portfolio. Essentially, higher income and lower duration are helping to make the case that bonds will have a much better 2022. While inflation and liquidity concerns remain, the median in a recent Bloomberg survey shows “dealers, strategists and economists project bond prices will rise modestly in tandem with cooling inflation, with the 10-year US note trading at 3.5% by end of next year.”

Finsum:A combination of higher income payments and lower duration has money managers becoming more bullish on treasuries.

Alternatives Poised for Huge Inflows According to Survey

According to a recent survey of active retail investors conducted by Opinium on behalf of Lansons, educating affluent investors on alternatives could lead to huge inflows. Lansons, a leading independent reputation management consultancy, partnered with strategic insights agency Opinium to conduct a nationally representative survey of 1,832 Americans. The survey found that a majority of Americans are unfamiliar with digital platforms that offer access to alternatives. Eighty percent have either never heard of these platforms or don’t know much about them. However, educating these investors could be the key to unlocking massive inflows as investors are certainly open to investing in them. Based on the results of the survey, 20% of Americans would strongly consider investing in alternatives and 7 percent are already planning to do so. In addition, active investors would be willing to allocate 25% of their portfolios, on average, to alternatives. These figures represent more than $1.3 trillion in potential investment. In addition, the current market conditions could provide an opportunity for the industry to educate investors about alternatives as nearly half (47%) of the survey respondents expressed extreme concern about the impact of inflation on their investments. Alternatives such as gold and real estate are generally considered hedges against inflation.

Finsum:If a lack of knowledge on alternative investing could be remedied, alternatives could see massive inflows.

Four Morgan Advisors Jump Ship to Wells

Wells Fargo continues to bolster its recruiting efforts with the addition of four Morgan Stanley advisors generating close to $5.6 million in annual revenue. The largest of the hires is Steven Esposito from Lake Forest, Illinois, who moved to Wells Fargo Advisors’ independent Financial Network channel. He managed $435 million in client assets and generated $2.8 million in annual production at Morgan. Esposito, a 39-year industry veteran, has worked at six firms, including Morgan Stanley for the past 14 years. Roni Murshad, a 20-year-industry veteran from Gaithersburg, Maryland, also made the move from Morgan to Wells FiNet. The advisor managed $79 million and generated $860,000 in annual production. Murshad, who began his career at Morgan Stanley in 2001, left after five years, and spent six years at Bank of America and Merrill Lynch, before returning to Morgan in 2012. In addition, two advisors from Westlake Village, California moved their team from Morgan to Wells Fargo. Howard Lee and Terri Lane managed $400 million and generated $2.1 million in annual production at Morgan. Lee started his career at Lehman Brothers in 1964, while Lane worked at six firms with stints at UBS and Bear Stearns, before joining Morgan Stanley.

Finsum:Wells Fargo bolsters its ranks with four Morgan Stanley advisors generating close to $5.6 million in annual production.